In a previous blog post, I covered how an early stage investor values a startup, but felt like there is likely more that can be said on the subject so consider this a ‘part 2’ to that blog post if you will. With the focus of this ‘part 2’ around how you can maximise your valuation and what are the drivers behind the boundaries of possible valuations for your company.

In my previous post, I covered how macro and geo contexts, amongst several factors, determine the relativistic value of a company to an investor on exit, and how traditional finance-driven valuations methods (DCF, etc) were inappropriate for early stage startups even if some of the elements that drive those finance-driven valuation methods were still applicable, such as expected revenues. I also covered how several factors about your company can influence what valuation you might be able to achieve. To kick off, let’s revisit those points.

The key drivers for maximising your valuation possibilities are:

- Excellent metrics. As different types of businesses have different types of metrics, the general point here is that numbers talk and.. Well you know how that expression goes. Do your numbers show strong customer interest? Do your numbers show a sustainable business? Do your numbers show your ability to bring in cash (within the timeframe that’s expected of your industry)?

- Excellent FOMO. What generates “fear of missing out”, or FOMO, is hard to pin down, but can usually be traced to elements that the founding team has, which when combined with what they are tackling, creates plausible ‘magic’. Whilst I believe most people that have the ability to create FOMO in others intrinsically, it is an art-form in understanding how others will perceive what you are working on and generating an honest trust in you and your team rather than relying on simple theatrics to try and achieve the same effect.

- Positive Macro-economic sentiment and confidence. As discussed in the previous blog post, these affect if investors will pay higher valuations now.

- Sector ‘hotness’. In effect, investor demand for what you do: the higher the demand the higher the valuation. Conjure up images of x.coin companies back in 2017 and you’ll know what I mean.

- The size of your raise: the bigger the raise the higher the valuation may need to be to avoid washing out the existing shareholders.

As I’ve written on metrics and FOMO before, I want to focus on the last three for this blog post.

In previous chapters I touched upon the basic fundraising equation:

[Money Raised / Post Money = % Dilution] or alternatively [Money Raised/% Dilution = Post Money], and “valuation” is typically used interchangeably used with “pre-money valuation” which is equal to [Post money — the Money Raised].The key element to consider with the above equation is that it’s not static. The variables that make up the equation change with time. These changes create higher and lower ranges that are acceptable for investors and founders, and below, we’ll cover how those come into play in more detail.

As covered before, It all starts with macroeconomic conditions and general sentiment in public markets. When things are going well, all companies rise, the index of stocks in a country rise, valuations rise, and the tolerance for buyers and investors to invest more and at higher valuations also rises. With all of that on the rise, at the earlier stages, this manifests itself by investors being able to tolerate increasingly more ‘expensive’ rounds, as in, rounds where they have to pay a higher valuation, because they see a possibility of selling their share of the company at a higher valuation in the future.

So, that’s the first point to make: in good times, investors are willing to increase post-money valuations. In bad times, this will no longer be the case, and if you want to read more on how to brace for that, I’ve covered it on how to weatherproof your business.

Secondly, the more mature the ecosystem, the more capital there is at play. As well as greater volume of money, there will be more specialised and sophisticated investors who can better judge the potential and therefore may pay more. The more investors and money around the table, the more competitive deals get, which will affect your valuation for the better. This is why it is easier to raise money at a higher valuation in California vs. an emerging ecosystem.

These two factors above imply that there is no ‘static’ view of valuation, rather, it’s dynamic, as it is affected by externalities.

Taking the above into consideration, the more constructive way of thinking of valuation is by thinking of it as an ‘acceptable’ or ‘probable’ range relative to the amount of capital you are raising.

This range has an upper and lower boundary, which bookend what your valuation could be. From an investor’s point of view:

The UPPER %-dilutions boundary– no early-stage investor is looking to take a majority stake of your business as that would likely constitute an acquisition, so you can easily remove taking 50% of your company at a round off the table. Therefore, your ‘real’ upper boundary is usually imposed on the investor by a few factors out of their control, including the competitiveness of the local ecosystem, the options of capital available to the founder, and how much the investor cares about how they could be perceived by other investors (some investors don’t care if they come across as predatory).

The LOWER %-dilution boundary -no investor is likely to give you money for free. As investors compete for your deal, they will be more keen on offering your more money for less dilution to you, but there is a limit. As investors do internal calculations on what is the minimum they need to return an investment to their investors (based on macro-conditions and expectations of the future of your company), there is a point where they simply can’t make the numbers work for them and they usually opt-out of offering you a deal if an alternative offer at a higher valuation (lower dilution) comes into the offers the founders are considering. Investors that understand your industry better will naturally have more tolerance towards higher valuations (eg, lower % dilution) as they can see the future potential of the company more clearly.

From a founder’s point of view, therefore, it’s about pushing towards a lower boundary through the variables you can control, eg. metrics, fomo, and round size (more to cover later).

Even though the boundaries above seem like they provide an endless amount of options, it actually sets the stage for a way of thinking of your company’s value… as a ‘range’ of options relative to the amount of capital you are raising instead of as a ‘fixed’ value.

So what’s an acceptable range then? Well if the range is dictated by macro conditions, then surely there is some sort of rule-of-thumb? Luckily there is, but it’s confusing as its different for angels vs. institutional investors and with new types of investors coming online (eg. pre-seed investors) that just adds more to the mix. However there is still a ‘range’ that you can use.

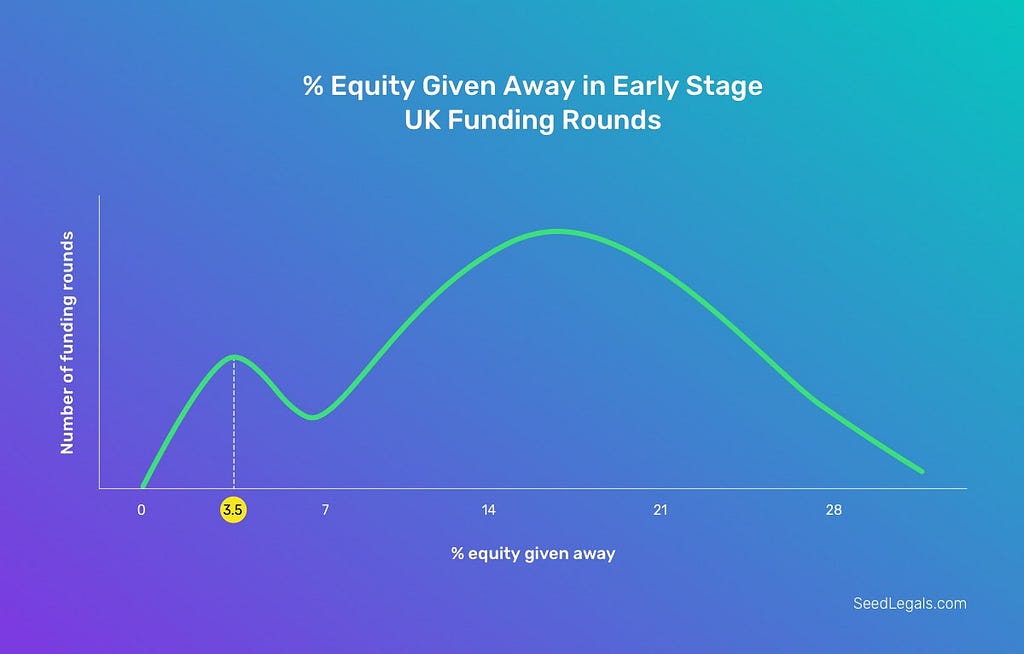

Seedlegals (a Seedcamp company) compiled some stats around valuations for pre-seed and seed rounds in the UK, for example, and this is the range they found (combined):

If you look at that gap (the tighter bit of it) and you say that it’s between 12% and 3.5% at the pre-seed stage and 25% to 12% to at the seed stage, you see that on average the ‘spread’ between the lower and upper boundaries on average is about 10%. To put that in context, if you were raising a 1m seed round, that would be the difference between a 3m valuation and a 7m valuation. Yes, it means a lot, but it also helps provide you with a workable range, and helps you contextualise what might be possible within ‘the norm’ (excluding crazy metrics or FOMO).

However, the 5th point I brought up that affects your valuation is the round size you go out to raise. As you can see, if I take the same range of dilution of 25%-12%, then a 2m round would generate a valuation range of 7m-15m. Quite the jump right? Simply put, as you can’t control the macro factors that determine the range you operate in, as a founder, you have total control over your round size, which is your primary tool in changing your valuation, along with showcasing strong metrics and developing the factors that can generate FOMO for your industry.

But It’s not simply about increasing your round size to exact the valuation range you want.. You will be evaluated for investment on what you’ve achieved and how you will effectively use the funds raised, so there is a point, where investors may very well think you’re raising too much for where you are, and that will be subjectively up to the discretion of the investor relative to your industry (and the implied valuation that that amount of cash will imply for them, more on that below).

In conclusion, you can’t control macro-economic conditions nor can you control how upper and lower boundaries change over time for investors, but you can control how much you are raising, and that affects your valuation just as much.

Extra Geek Math on how to find a round size range based on the above — If you want to figure out what a probable round size for your company could be, AngelList host a valuation range by $ here — https://angel.co/valuations Mapped with the % dilution range from Seedlegals, you can backwards solve for what acceptable ranges might be. For example, for London, AngelList’s calculator says that the average valuation is $3.3m. If you assume that represents the pre-money and you solve for round-size, assuming the range of between 25% and 12% as per the above examples, and with some algebra to solve for round size, you end up with a viable round size of between $680K and $1.6M on average as per the data. Can you do better than that? For sure, but now you know how to calculate it!

Special thanks to Devin Hunt & Stephen Allott for helping me proof-read this post!