One of the key lessons you learn in startup life quickly is: you measure what matters and then make decisions from that. OKRs, and KPIs are born from this philosophy.

However, we are all equally well versed in the dark side of this, where one wrong KPI can lead to a worse outcome for all. The classic example of this is incentivising a sales team to sell as much as possible, but not qualifying customers and therefore you end up having runaway costs to acquire customers and churn can sky rocket after. Few companies do that these days, but it’s just to make the point: Wrong metrics can kill.

In an investment fund, there are several metrics you track, the obvious ones are based on ‘return on capital invested’ and similar cash-based metrics. These make sense, but have some ‘lag’ to them as usually companies, for early stage funds in particular, take time to mature. As such, some LPs choose to focus on deal-attribution to gauge how good the fund will be. In effect: Which partner led what deal.

So, basically, the implication is, if you had a team where everyone was a Lionel Messi…. voila, you’d have an amazing team! What likely isn’t appreciated in that logic, is that a team of investment partners where everyone is an Lionel Messi doesn’t quite equate to more successes because partners play many roles in supporting each other, not just shooting for points, so to speak.

I believe the above logic of partner attribution creates several problems that plague our industry and funds. These include:

Inhibits team collaboration — As with most team sports, investment partnerships require good team work to enable wins. People need to ‘pass the ball’ to the best player to help score, whether that’s with helping a founder with an issue or a connection, or dealing with a legal technicality that one partner knows best, collaboration wins in the long run.

Creates deployment budget pressure and quarrels between partners — If you know that a winning bet is what gets you credit, how do you make sure people aren’t over indexing on as many bets as possible? How do you get your partners to think of the fund’s budget as a whole not as a portion that they will make successful?

Inhibits pairing the ideal partner with the founder depending on the founder’s needs — Similar to the first point, people start playing in silos.

Inhibits the ‘evolution’ of the relationship with the founder — Different partners in a fund can be better for the founder at different stages in the founder’s journey. Say one partner was super experienced with growth stage issues because of their previous job.. if you had a partner attribution model, you’d be prevented from this kind of transition.

Creates cults of personality in partners– Success can bring with it a dark side for some, and by not having a way to spread success across your team, you run the risk of creating bottlenecks in your fund’s brand attributable to one person.

So how do you make sure that if you adopt the above you don’t have a team of lacklustre partners then? Well that’s when the partnership needs to be solid enough to be open and frank with each other when a partner isn’t living up to expectations and helping them improve.

Seedcamp has evolved over the years, but one thing we did early on was embark on the path of not attributing deals to individual partners because we work as a team with our founders. It gets tricky to navigate at times, largely in conversations with investors, media and award structures where they are looking for that one person to attribute to or comment on a deal, but that’s not how we operate at seedcamp. It takes a village to support a founder and we are steadfast in our belief that bringing the right people in from across our partnership, team and network not only removes ego of the individual but ensures we work collaboratively to help our founders achieve excellence.

Investors frequently get a bad rap for how they communicate between themselves and more importantly, with the founders they back, but luckily this is changing globally at a rapid pace and today more and more founders and investors communicate as peers.

Whilst no one is perfect, part of the reason this bad rap happens, is due to a lack of contextual empathy (understanding the circumstances the other person might be in) and perceived power dynamics between investors and founders. In effect, it’s easy to be rude when you think the other person should tolerate it, and this can go both ways (and frequently and increasingly does).

However, this doesn’t just apply to Investor/Founder relationships. It can apply across all sorts of relationships, in particular ones where one person feels obliged to give feedback, and that’s the key commonality here, having to provide a perspective to another person.

A tried and time tested method that’s been glued to many a high-schooler’s classroom walls is the THINK method of providing feedback. It’s ironic that something so commonly found in our institutions of education is often so ignored when sharing key information with those we work with.

THINK (before you speak) stands for:

T — is it True? — sometimes thoughts are more ‘perceptions’ rather than facts H — is it Helpful? — sometimes it helps you to unload more than it does to the recipient to ‘receive’ I — is it Inspiring? — the opposite, ‘is it depressing’ clearly doesn’t do much for me, suspect that applies to many of us N — is it Necessary? — we’re all busy and we’re challenged in some way, so is this something that’s absolutely critical? K — is it Kind? — People tend to remember how you made them feel more than if you were right, and people tend to remember this for a long long time

If it didn’t ruin the acrostic, I’d add another ‘T’ to the list for ‘is it the right time?’ — pick the right time to give feedback, not when rushed or when emotions are running high.

Another factor to also consider prior to giving any feedback, is whether or not you’re the right person to be providing the feedback or if someone else in your team might be better suited to do so based on their relationship (and/or experience) to the person you are talking to.

The key things that stand out for us to keep in mind from the above list and in the context of the startup world, where so many things are in flux so quickly for all parties involved, is gauging how best to communicate an opinion you might have in light of it, at best, being one of multiple opinions on how to tackle something and how quickly things can change.

Don’t beat yourself up if you get “THINK”ing wrong from time to time, we all make mistakes in each one of these each time, but hopefully THINKing ahead might spare you a ruined relationship going forward and actually help you move ‘forward’ on what you’re both trying to achieve.

Making decisions are part of the day-to-day at any startup or investment fund. However, how those decisions are made varies greatly. Decision making within an organisation can range from hyper-gut-feel to hyper structured and rigid.

Whilst I don’t profess to be an expert on the subject, having now done over 350+ investments, one of the areas we needed to innovate to scale was around was how to best make good decisions efficiently and quickly. On this post I want to review some of the ones I use within Seedcamp to help drive speed of decision making but also quantify and qualify possible choices for subsequent decisions.

To start with, when coming up with or choosing a decision making process, it helps to know what kind of outcome you want and when. Sometimes you THINK you want an absolute outcome (more on that in a second), but in reality you might benefit from having a stage before it that assists your absolute outcome by grouping possible choices into relative outcomes first, followed by the absolute choice.

To help explain the difference between absolute and relative, I’ll share the two types, and the variants we use internally:

Relative Processes — these processes are ones where there is no need to make a decision at the end of it, but where elimination of those options you don’t want, helps reduce the time you spend discussing real options of consideration later. Of course, you can use these for choice-making as well, but these don’t work well if there is only one decision to make without other choices.

Our relative processes include:

1.1 Currency points system — when we want to collate the opinion of various people, this system works well. The larger the group the better this works too. Basically, the idea is simple, everyone is given a budget of ‘points’, we use ‘9’ but as long as it’s easy and odd it helps reduce too much burden (too big) or not enough granularity (too small). With these 9 points you can ‘spend’ them outcomes you prefer, whichever way you want. Say if you want to ‘spray and pray’ you could give 1 point to all the choices. However, most people tend to group their use of points into either high conviction (lots of points to a few) or a smallish cluster. You then weight two outcomes — the choices determined by the most points, and the choices that may have not got the most points, but that most people gave any points two. They are both interesting to discuss.

example: 5 choices, 2 get the most points, 3 get the most votes (at least one). The chat to have is, are the 2/3 the same? what’s the difference between the most popular one (most votes) and the most convicted one (most points)?

1.2 Attribute based stack system — - Similar to the above, this format’s ultimate objective is to create a top to bottom list of options from best to worst, however on this one, it is done on the basis of attributes that each choice has. For example, if we were talking about cars, it would be how each car fared on gas mileage, speed, etc, and then for each of these, from 1–5 how they did in each attribute. You then take the average score and stack and rank accordingly across the attributes so you can see how choices stack up across each. The key thing is to make sure you’re choosing the right attributes to focus on, otherwise it’s garbage in and garbage out. For some of our investment decisions, for example, we put extra weight on team related attributes as that correlates highly with success in our experience.

example: car 1, 2, and 3 have mpg, top speed, cost, and maintenance fee. If cost is the most important attribute, how do the cars stack up on the rest of the attributes?

2. Absolute processes — these processes help organise the information that is spread out across the team to provide one choice, but strip the team of a view of where an opportunity or decision sits in the universe of choices and usually works well in decision making where you don’t have multiple choices to choose from, rather one decision to make, yes or no.

Our absolute processes include:

2.1 The Gap Points system— In order to force a decision within the team, we ask people to give a company a score from 0–10, but it cannot be 4,5,6 and the average of the team’s score has to be greater than 7.5 for us to really consider the option as viable. In effect, this allows the team to not cluster around hedged opinions, rather the system forces a polarity and also an extra level of commitment by someone to really get a decision over the line.

example: the team has identified a possible yes or no decision, and no further debate on attributes is helpful. A vote is required which synthesises people’s attributes into one score. Assume a team of 4. One votes 3, one 9, one 7, and one 7.5. The average is 6.63 (which as is below a 7.5 is a ‘no’), but that matters less than the obvious which is that most of the team is lukewarm about it, and one is vaguely supportive. This can expedite the true nature of the debate internally.. why is one person a no and one a strong yet and two stuck in the middle?

2.2 The Team Momentum System — Sometimes the issue isn’t whether or not the decision is clear due to a thorough analysis, rather it’s that too many people are involved and therefore it generates too much debate. This system moves things to relying on a critical group to drive momentum. As part of this system you reduce the people that are accountable for a decision and then the remaining team members are consulted, but with a view unless there is a strong no at the end of a final review, that the default answer is yes. Naturally there needs to be a high degree of trust and you need to make sure there is no ‘factionalisation’ of team members or otherwise you effectively circumvent the value of the system.

example: Two team members passionate about a sector, say HR-tech, engage with a company and both build conviction on a company, the remaining team members would each have a chance to veto a ‘default yes’ from those that have researched it, but likely they only would for some externality rather than a view on a sector that they’re not exploring themselves.

2.3 Lastly, ThePizza System is a variant of the above but requires more planning as its one where ‘we collectively cut the pizza, but someone picks the slice’— In effect, the team agrees on a predetermined criteria that qualifies a decision as viable and then someone has the ability to drive the decision through conviction, so everyone is happy with the outcome based on the criteria, but one person drives it to a yay or nay, which reduces analysis paralysis.

example: If the entire team agrees that any company that is in the space of solar technology that is capital efficient will automatically trigger a yes/no debate. In effect, you have decided which way something gets chosen for either final decision or final discussion.

As I said before, any one of these systems absolute or relative, can work for just about any decision you want to make, but the key to really improve efficiency within a mix of team sizes and severity of the decision making is knowing which system helps you move things along prior to having to debate things with your team. Don’t limit yourself to just one system, if you benefit from it, stage them to help reduce cognitive load prematurely as it can fatigue a team’s discussion time and can polarise choice prematurely. If you have a variety of choices prior, come up with a way of using a relative system before an absolute system is applied.

To illustrate the above, at Seedcamp, we usually have to make lots of decisions, but it’s hard to treat each choice as an absolute choice, so one of the things we do is set up a curation process by first using a relative decision system, which then allows us to focus our debate time on those choices that surface to the top only, and then once we have a narrower group, we switch to an absolute decision system for making final decisions.

The expression “elephant in the room” (usually “the elephant in the room”) is a metaphorical idiom in English for an important or enormous topic, problem, or risk that is obvious or that everyone knows about but no one mentions or wants to discuss because it makes at least some of them uncomfortable or is personally, socially, or politically embarrassing, controversial, inflammatory, or dangerous.

It is based on the idea/thought that something as conspicuous as an elephant can appear to be overlooked in codified social interactions and that the sociology/psychology of repression also operates on the macro scale. Various languages across the world have words that describe similar concepts.

I love this expression because it’s so obvious…how could you NOT notice something so big within a confined space… and yet, sometimes we do ignore it, or at least fail to acknowledge it; When it comes to pitching your company, it’s not unusual for you to have an ‘Elephant in the Room’ and, funnily enough, it’s often easier to ignore it (out of fear) rather than confront it head on.

Why is this important?

Frequently, your ‘Elephant’ is something that’s perhaps awkward to be up front about, such as a like-for-like competitor already in market; or that several companies like yours have failed in the past, or that there is a big player out there who owns most of the market.

I’ve received many presentations over the years and also observed how others hear and perceive them and what inevitably happens is when you ignore that ‘Elephant’, it grows in your audience’s mind. It grows to the point where it consumes their entire mind space and the points you are trying to make get lost because the audience is actively trying to suppress their desire to counter with ‘how about xxx” which has been festering in their minds all this time!

Whether you address it directly or indirectly, you need to address it sooner rather than later. The solution is simple: you have to realise that this elephant isn’t real. It’s merely a blow up Elephant and one you can deflate easily if addressed early on in your presentation. People will either agree with the way you deflated it or not but you’ll at least be able to move past it.

How do you identify your Elephant?

Unless you are willing to delude yourself, you likely already know what it is. It may be a question investors or friends have repeatedly asked you when you explain what you are working on. It usually starts with something like ‘isn’t that like…’ or ‘didn’t that…’ or something like that. In short, if you are feeling uncomfortable about something, most likely that’s your Elephant.

How do you deflate your Elephant?

Through logic. The fact is, you would not have started working on your business if you didn’t have good reason to believe this ‘Elephant’ was not going to hurt you in the long-run. If it’s a competitor everyone asks you about, you can simply talk about how you feel you are tackling things differently and serve a different need/customer. If it’s a sector that has had many deaths in the past, perhaps talk about how the timing is different now vs. then, and really delve deep into why that is the case. For example, one of our companies, Thriva, helps you take control of your health and find out what’s happening inside your body with a simple finger-prick blood test. When they went out to pitch, it was around the time Theranos was imploding, and there was enough ‘perceived’ similarities, that pitching without addressing that case as specifically different (and how) simply led to the eventual burst later by someone with the obvious question. Naturally, the founder was on to this, and addressed all the key points of differentiation early on.

In conclusion, to move past an Elephant, you simply need to have a sound logic as to why the Elephant doesn’t apply to you; any reason is better than no reason at all!

In a previous blog post, I covered how an early stage investor values a startup, but felt like there is likely more that can be said on the subject so consider this a ‘part 2’ to that blog post if you will. With the focus of this ‘part 2’ around how you can maximise your valuation and what are the drivers behind the boundaries of possible valuations for your company.

In my previous post, I covered how macro and geo contexts, amongst several factors, determine the relativistic value of a company to an investor on exit, and how traditional finance-driven valuations methods (DCF, etc) were inappropriate for early stage startups even if some of the elements that drive those finance-driven valuation methods were still applicable, such as expected revenues. I also covered how several factors about your company can influence what valuation you might be able to achieve. To kick off, let’s revisit those points.

The key drivers for maximising your valuation possibilities are:

Excellent metrics. As different types of businesses have different types of metrics, the general point here is that numbers talk and.. Well you know how that expression goes. Do your numbers show strong customer interest? Do your numbers show a sustainable business? Do your numbers show your ability to bring in cash (within the timeframe that’s expected of your industry)?

Excellent FOMO. What generates “fear of missing out”, or FOMO, is hard to pin down, but can usually be traced to elements that the founding team has, which when combined with what they are tackling, creates plausible ‘magic’. Whilst I believe most people that have the ability to create FOMO in others intrinsically, it is an art-form in understanding how others will perceive what you are working on and generating an honest trust in you and your team rather than relying on simple theatrics to try and achieve the same effect.

Positive Macro-economic sentiment and confidence. As discussed in the previous blog post, these affect if investors will pay higher valuations now.

Sector ‘hotness’. In effect, investor demand for what you do: the higher the demand the higher the valuation. Conjure up images of x.coin companies back in 2017 and you’ll know what I mean.

The size of your raise: the bigger the raise the higher the valuation may need to be to avoid washing out the existing shareholders.

As I’ve written on metrics and FOMO before, I want to focus on the last three for this blog post.

In previous chapters I touched upon the basic fundraising equation:

[Money Raised / Post Money = % Dilution] or alternatively [Money Raised/% Dilution = Post Money], and “valuation” is typically used interchangeably used with “pre-money valuation” which is equal to [Post money — the Money Raised].

The key element to consider with the above equation is that it’s not static. The variables that make up the equation change with time. These changes create higher and lower ranges that are acceptable for investors and founders, and below, we’ll cover how those come into play in more detail.

As covered before, It all starts with macroeconomic conditions and general sentiment in public markets. When things are going well, all companies rise, the index of stocks in a country rise, valuations rise, and the tolerance for buyers and investors to invest more and at higher valuations also rises. With all of that on the rise, at the earlier stages, this manifests itself by investors being able to tolerate increasingly more ‘expensive’ rounds, as in, rounds where they have to pay a higher valuation, because they see a possibility of selling their share of the company at a higher valuation in the future.

So, that’s the first point to make: in good times, investors are willing to increase post-money valuations. In bad times, this will no longer be the case, and if you want to read more on how to brace for that, I’ve covered it on how to weatherproof your business.

Secondly, the more mature the ecosystem, the more capital there is at play. As well as greater volume of money, there will be more specialised and sophisticated investors who can better judge the potential and therefore may pay more. The more investors and money around the table, the more competitive deals get, which will affect your valuation for the better. This is why it is easier to raise money at a higher valuation in California vs. an emerging ecosystem.

These two factors above imply that there is no ‘static’ view of valuation, rather, it’s dynamic, as it is affected by externalities.

Taking the above into consideration, the more constructive way of thinking of valuation is by thinking of it as an ‘acceptable’ or ‘probable’ range relative to the amount of capital you are raising.

This range has an upper and lower boundary, which bookend what your valuation could be. From an investor’s point of view:

The UPPER %-dilutions boundary– no early-stage investor is looking to take a majority stake of your business as that would likely constitute an acquisition, so you can easily remove taking 50% of your company at a round off the table. Therefore, your ‘real’ upper boundary is usually imposed on the investor by a few factors out of their control, including the competitiveness of the local ecosystem, the options of capital available to the founder, and how much the investor cares about how they could be perceived by other investors (some investors don’t care if they come across as predatory).

The LOWER %-dilution boundary -no investor is likely to give you money for free. As investors compete for your deal, they will be more keen on offering your more money for less dilution to you, but there is a limit. As investors do internal calculations on what is the minimum they need to return an investment to their investors (based on macro-conditions and expectations of the future of your company), there is a point where they simply can’t make the numbers work for them and they usually opt-out of offering you a deal if an alternative offer at a higher valuation (lower dilution) comes into the offers the founders are considering. Investors that understand your industry better will naturally have more tolerance towards higher valuations (eg, lower % dilution) as they can see the future potential of the company more clearly.

From a founder’s point of view, therefore, it’s about pushing towards a lower boundary through the variables you can control, eg. metrics, fomo, and round size (more to cover later).

Even though the boundaries above seem like they provide an endless amount of options, it actually sets the stage for a way of thinking of your company’s value… as a ‘range’ of options relative to the amount of capital you are raising instead of as a ‘fixed’ value.

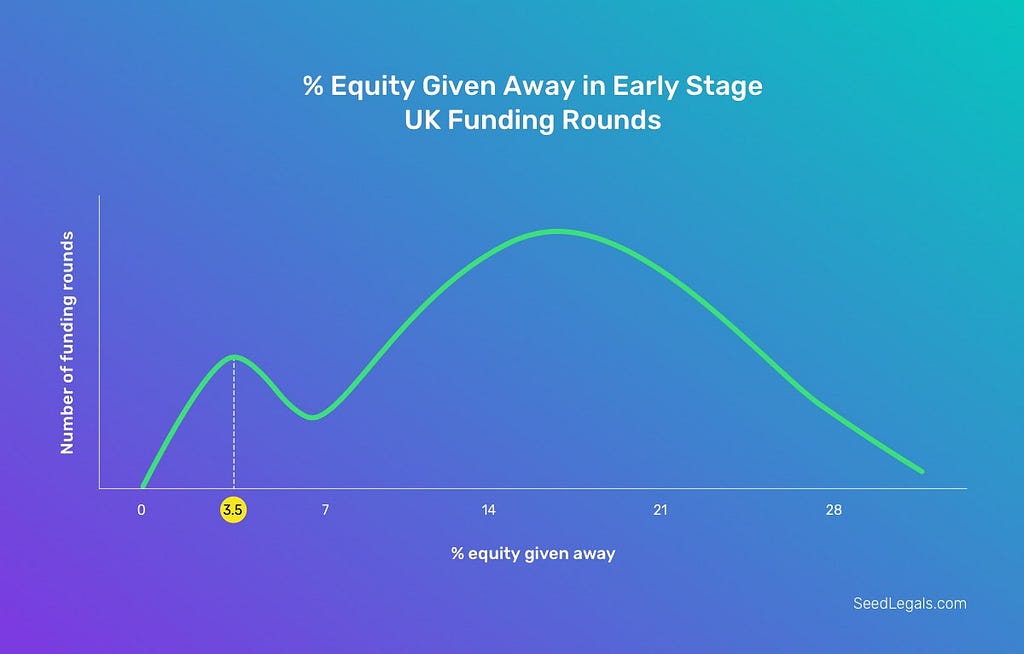

So what’s an acceptable range then? Well if the range is dictated by macro conditions, then surely there is some sort of rule-of-thumb? Luckily there is, but it’s confusing as its different for angels vs. institutional investors and with new types of investors coming online (eg. pre-seed investors) that just adds more to the mix. However there is still a ‘range’ that you can use.

If you look at that gap (the tighter bit of it) and you say that it’s between 12% and 3.5% at the pre-seed stage and 25% to 12% to at the seed stage, you see that on average the ‘spread’ between the lower and upper boundaries on average is about 10%. To put that in context, if you were raising a 1m seed round, that would be the difference between a 3m valuation and a 7m valuation. Yes, it means a lot, but it also helps provide you with a workable range, and helps you contextualise what might be possible within ‘the norm’ (excluding crazy metrics or FOMO).

However, the 5th point I brought up that affects your valuation is the round size you go out to raise. As you can see, if I take the same range of dilution of 25%-12%, then a 2m round would generate a valuation range of 7m-15m. Quite the jump right? Simply put, as you can’t control the macro factors that determine the range you operate in, as a founder, you have total control over your round size, which is your primary tool in changing your valuation, along with showcasing strong metrics and developing the factors that can generate FOMO for your industry.

But It’s not simply about increasing your round size to exact the valuation range you want.. You will be evaluated for investment on what you’ve achieved and how you will effectively use the funds raised, so there is a point, where investors may very well think you’re raising too much for where you are, and that will be subjectively up to the discretion of the investor relative to your industry (and the implied valuation that that amount of cash will imply for them, more on that below).

In conclusion, you can’t control macro-economic conditions nor can you control how upper and lower boundaries change over time for investors, but you can control how much you are raising, and that affects your valuation just as much.

Extra Geek Math on how to find a round size range based on the above — If you want to figure out what a probable round size for your company could be, AngelList host a valuation range by $ here — https://angel.co/valuations Mapped with the % dilution range from Seedlegals, you can backwards solve for what acceptable ranges might be. For example, for London, AngelList’s calculator says that the average valuation is $3.3m. If you assume that represents the pre-money and you solve for round-size, assuming the range of between 25% and 12% as per the above examples, and with some algebra to solve for round size, you end up with a viable round size of between $680K and $1.6M on average as per the data. Can you do better than that? For sure, but now you know how to calculate it!