SeedCamp’s hackathon, Seedhack, took place at Google Campus, London, on the 8th to 10th of November. It brought together some of the brightest talent in the startup community from 15 countries with one of the best accelerator programs in the world and mashed it up with awesome content providers like Twitter, Facebook, BSkyB, BBC, Getty, HarperCollins, EyeEm, Nokia Music and Imagga. There were a total of 12 teams working on interesting and exciting projects.

As part of this hackathon, Ali and Will helped me aggregate resources to help founders better understand the process of raising equity and the impact it can have to their founder stakes. We aggregated resources to help entrepreneurs to understand the numbers and implications of raising money and giving out equity. Valuing a company and calculation its impact on your equity is a very complex and confusing for entrepreneurs as well as being far from an exact science, this is the pain point that we wanted to address.

In the words of Seedhack attendee Will Martin (@willpmartin)

“Fundraising is one of the most difficult parts of the startup world, as first time founders this is an even more daunting process. Experience of raising a round and understanding the numbers and implications of that round and the related equity issued to an investor as well as employees in the form of an option pool is vital, but sadly is only fully understood by going through the process for real. Our intention was to give founders the knowledge required by being able to go through the process in a simple and easy way, thus giving the founder the confidence when it happens for real.

Ali and I are first time founders currently actively looking for investment. We know the total value we need in terms of money we want to raise as well the percentage of equity we are comfortable willing to give up to the investor. What we didn’t know and learned through the process is the implications in future rounds as a result of that initial funding round. Having an option pool for employees, advisors, board members etc. is something that complicates the issue and is often a requirement in the terms an investor is offering. This complicates the issue for the founder, so being aware of the impact of their shareholding as a result is vital for a founder as it is them that gets diluted in the first round but also any subsequent round, but it is often overlooked.

The changes to equity positions of the founders, investors, employees etc. is very important to understand as it dictates control and value of a company. Having this knowledge now gives us as founders a huge advantage over other founders we are competing with for funding and bridges the knowledge gap that exists for first time founders.”

In order to read some of the terms on this cap table model, below are some definitions which you might find useful:

Pre & Post Money Valuation –

“The pre-money valuation is the valuation that a company goes into raising a round of financing with. By establishing this valuation, it helps investors understand what amount of equity they will receive in the company in exchange for their capital. Once the financing round has been completed, the post-money valuation is the sum total of the pre-money valuation plus the additional capital raised. So, if the pre-money valuation of a company is $10 million and they raise $2.5 million from investors, their post-money valuation would be $12.5 million. Investors would own 20% of the resulting company.” – Dave Morin, Source Quora

“A PRE-MONEY VALUATION is the valuation of a company or asset BEFORE investment or financing. If an investment adds cash to a company, the company will have different valuations before and after the investment. The pre-money valuation refers to the company’s valuation before the investment.

External investors, such as venture capitalists and angel investors will use a pre-money valuation to determine how much equity to demand in return for their cash injection to an entrepreneur and his or her startup company. This is calculated on a fully diluted basis.

If a company is raising $250,000 in its seed round and willing to give up 20% of their company the pre-money valuation is $1,000,000. (250,000 * 5 -250,000 = 1,000,000)

Formula: Post money valuation – new investment

Source – http://en.wikipedia.org/wiki/

A POST-MONEY VALUATION is the value of a company AFTER an investment has been made. This value is equal to the sum of the pre-money valuation and the amount of new equity.

The Post-money valuation is the sum of the pre-money valuation and the money raised in a given round. At the close of a round of financing, this is what your company is worth (well, at least on paper).

If a company is worth $1 million (pre-money) and an investor makes an investment of $250,000, the new, post-money valuation of the company will be $1.25 million. The investor will now own 20% of the company.

The only reason it’s worth spending time on this term at all is that it “sets the bar” for your future activities. If your post-money after your first round of financing is $4 million, you know that to achieve success, in the eyes of your investors, any future valuations will have to be well-in-excess of that amount.

Formula: New Investment * total post investment shares outstanding/shares issued for new investment. “

Source – http://en.wikipedia.org/wiki/

Option Pools –

“An option pool is an amount of a startup’s common stock reserved for future issuances to employees, directors, advisors, and consultants.” – from startuplawyer.com

Option pools can also be formed by Restricted Stock Units, but whichever one you use, they are generally still called ‘Option Pools’.

The OPTION POOL is the percentage of your company that you are setting aside for future employees, advisors, consultants, and the like. Employees who get into the startup early will usually receive a greater percentage of the option pool than employees who arrive later.

“The size of the Option Pool as a percentage of the POST-MONEY Valuation and where ALL of it comes from the founder’s equity. This is the least founder-friendly way to present this, but it is also the point at which most early stage investors will start the negotiations. The expectation from traditional venture firms is that this will equal 15%-25% of the company AFTER they make their investment. The Option Pool is one of the most complex and, from the entrepreneur’s perspective, confusing terms in an equity financing scenario.” – source http://www.ownyourventure.com/

Round Size –

The investment, or money is how much money is raised in a given round of financing. However, the decisions (and their implications) surrounding this number are among the most important that a founding team makes. It is not just about how much money is raised, it is about the terms that the money is raised on and, maybe most importantly, whose money it is and what they bring to the table in addition to money. – Source http://www.ownyourventure.com/

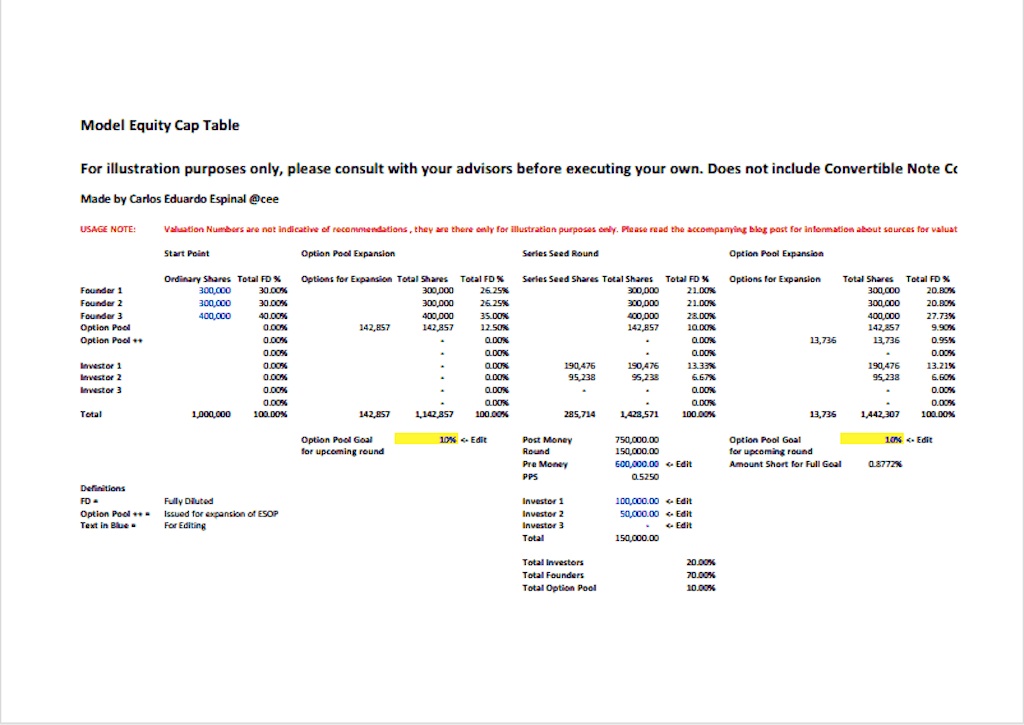

Link to the Model Cap Table: http://bit.ly/1ayKk8p

NOTE FOR MODEL TO WORK – It needs to run on Excel (Google docs coming soon) and with circular calculations turned on. This can be done by going to (Mac Excel) Preferences -> Calculation -> Iteration -> Click on Limit Iteration

If you are considering using Convertible Notes as part of your round, check out this variant of the cap table with notes on how to convert as well: http://bit.ly/17kHlSA

Additional Equity Calculation Tools (Thanks to Ali Tehrani for finding these – @tehranix) –

- Equity dilution calculator from Smart Asset: https://www.smartasset.com/

infographic/startup - Dilution inforgraphic from Mark Suster: http://www.

bothsidesofthetable.com/2011/ 10/14/understanding-how- dilution-affects-you-at-a- startup/ - Comprehensive book on Venture capital by Brad Feld and Jason Mandelson: http://www.amazon.com/Venture-

Deals-Smarter-Lawyer- Capitalist/dp/0470929820/ref= sr_1_1?ie=UTF8&qid=1311546351& sr=8-1 - Smart Sim Equity Simulator – http://ownyourventure.com/

equitySim.html

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 3.0 Unported License.

Related articles

1 Comment